How Canada Turned Housing from Shelter into Scarcity

Chapter 1 — The Illusion of Housing Wealth

A house can rise in price without becoming proportionally more useful, which means housing inflation is not the same thing as real wealth creation.

A house can double in price without becoming twice as useful.

That is the first fact the modern housing debate keeps trying not to see. A detached house in Toronto or Vancouver does not suddenly shelter two families instead of one because its market value rises. Its walls do not become sturdier. Its roof does not become more weatherproof. Its plumbing does not become more advanced. A kitchen renovation can add some value. A finished basement can add some value. A genuinely improved structure can become more useful. But that is not what explains the great housing repricing of the last generation. In the most distorted markets, the startling increase in value did not come mainly from making better homes. It came from owning access to increasingly scarce land.[5]

That distinction is the beginning of this book.

For many people, rising house prices feel like rising wealth because, at one level, they are rising wealth. Net worth statements improve. Home equity grows. Owners feel more secure.[3][4] Banks lend against appreciated value. Families begin to imagine retirement, inheritance, or emergency stability through the house they already own. On paper, the country looks richer. Neighbourhoods that were once merely ordinary begin to appear prosperous because the numbers attached to their homes are larger.

But paper wealth and real wealth are not the same thing.

A society becomes richer in the deepest sense when it produces more goods, more services, more useful capacity, more infrastructure, more knowledge, more tools, more homes that people can actually live in. That is real wealth: an expansion of what a country can do, make, maintain, and provide. If ten thousand new homes are built, that is real additional housing wealth. If a neighbourhood is serviced, expanded, and made capable of accommodating more people at decent cost, that is real additional capacity. If a home is substantially improved and made more durable or more functional, some of its increased value reflects real added usefulness.

But if the same house simply becomes more expensive because access to comparable homes has become more restricted, then something different is happening. The owner may indeed become wealthier on paper, but the society as a whole has not necessarily produced an equivalent new asset. In many cases it has only repriced access.

That is why housing inflation has such a strange moral and economic quality. It creates gains for some people that are very real in private balance-sheet terms, while simultaneously making entry more difficult for others. One household experiences a windfall. Another experiences exclusion. One generation sees its home transform into a nest egg. Another sees the same market transform into a gate it may never cross. The wealth is not wholly imaginary, but neither is it purely productive. It is partly redistributive. It moves advantage toward those who were already inside.

This is where a crucial distinction has to be made early: between the structure and the land beneath it.

A house has two major components of value. One is the structure itself: the lumber, concrete, wiring, windows, roof, insulation, labour, and workmanship that make the building usable. The other is the site: the location, the land, and, most importantly, the legal and political permission embedded in that land. In a normal production system, the structure matters a great deal. A larger, newer, or better-built home is worth more because more was actually created. But in a scarcity-distorted system, the land component begins to dominate. The value rises not because the house became much better, but because the right to occupy that location, in that jurisdiction, under that set of land-use constraints, became more scarce.[5][10][11]

That is why an aging bungalow can become a million-dollar asset while remaining, in physical terms, an aging bungalow.

This point matters because the public language around housing constantly blurs it. Politicians talk about rising home values as though they are straightforward evidence of national prosperity. Existing owners are encouraged to treat appreciation as proof of sound economic management. Financial institutions treat housing wealth as collateral and reassurance. Even media language often slides quietly from “prices are up” to “wealth has been created.” But what kind of wealth has been created if the central fact is that the same stock of shelter now costs more to access?

The answer is uncomfortable. A portion of what gets called housing wealth is really the monetization of scarcity.

That does not mean every gain is fake. It does not mean every owner is deluded. It does not mean houses should have no investment dimension at all. Real homes are real assets. Improvements matter. Locations matter. Cities can become more productive and more desirable. But once price escalation far outruns the improvement of the underlying structure, the growth of wages, and the ordinary capacity to build comparable housing, something more troubling has entered the system.[1][5] Wealth is no longer being measured mainly by what has been added. It is increasingly being measured by what has been fenced off.

A simple proof anchor helps keep the distinction clear. If a home’s price rises mainly because the structure became larger, better, or more durable, the gain reflects something that was actually added. But if prices across major markets rise much faster than ordinary earnings, far faster than the underlying structure improves, and far beyond what comparable replacement would suggest, then a larger share of value is coming from scarcity, location, and permission rather than from newly created usefulness.[1][5] The house may still be an asset. The question is what kind of asset it has become.

That is why housing inflation is so politically confusing. It allows the same phenomenon to be experienced as success and failure at once. To the owner who bought twenty years ago, the system seems to reward prudence, patience, and stability. To the younger household trying to enter, the same system looks arbitrary, punitive, and rigged. To the city government, rising assessment values may look like a stronger tax base. To the renter, they look like a future disappearing. To the country as a whole, rising nominal real-estate wealth can look like prosperity. To anyone asking whether more abundant and secure housing has actually been created, the answer is far less impressive.

This is why the housing crisis is such a powerful entry point into a larger argument. It is visible. It is emotionally legible. It reaches directly into ordinary life. People may disagree about interest rates, zoning, capital flows, monetary policy, urban design, or macroeconomics. But they understand what it means to watch a modest house become unaffordable without becoming meaningfully better. They understand what it means to feel that the number attached to shelter has become detached from shelter itself.

And once that detachment becomes visible, the next question becomes unavoidable.

Was housing always like this?

If the answer were yes, then this would simply be the permanent condition of urban life, unfortunate but unsurprising. But if the answer is no — if housing once behaved more like something a society could produce, and only later began behaving more like a scarce asset whose price rose faster than its usefulness — then the problem is deeper than speculation, mood, or bad luck. It means a structural break occurred somewhere in the system.

This chapter does not claim to explain the entire housing crisis. Its task is narrower. It establishes the right starting point: not abstract theory, not party politics, and not philosophical grievance, but the surface reality that a house can become vastly more expensive without becoming proportionally more valuable in any real productive sense.

The claim would weaken if rising prices had mainly tracked large improvements in the housing stock itself — better structures, much higher replacement value, or a broad expansion of abundant new housing delivered at ordinary cost. In that case, appreciation would look more like the pricing of real added capacity. But where the same shelter grows radically more expensive without comparable added usefulness, the scarcity reading becomes harder to avoid.

Once that is clear, the reader is ready for the first real historical puzzle of the book.

If rising prices are not the same as rising real wealth, then when did housing stop behaving like a more ordinary good and begin behaving like this?

Chapter 2 — When Housing Stopped Behaving Normally

Housing once behaved more like a normal production good and later began behaving more like a scarcity asset.

For long stretches of the twentieth century, housing behaved more like a normal production good.

That does not mean it was always cheap. It does not mean every city was easy, every family could buy comfortably, or every decade was free of local booms and shortages. It means something narrower and more important. Over long periods, housing prices remained more closely tied to the practical world of making housing: wages, construction costs, serviced land, and the ordinary ability of supply to respond when demand rose.[1][5][10][11] The system was not perfect, but its logic was recognizable. More people needed homes, prices rose, builders built, and at least some of the pressure was translated into more housing. That older pattern is the baseline that modern debates keep forgetting.

The reason it matters is simple. Most housing arguments begin too late.

They begin in the 2000s, when the crisis already looks obvious. Prices are already running ahead of incomes. Down payments are already absurd. Younger households are already being shut out. Then the search for causes starts in whatever is most visible in that moment: low interest rates, cheap credit, investors, immigration, foreign capital, speculation, urban popularity. Some of those forces are real. Some matter a great deal. But if housing had already begun to behave differently before those explanations reached full force, then they cannot be the whole story. They may be accelerants. They may be amplifiers. They may be the forces that made the crisis impossible to ignore. But they are not necessarily the deepest break.

That is the puzzle of this chapter.

The simplest way to state it is this: housing once behaved more like something a society produced, and later began behaving more like something a society rationed.[1][5][10][11]

That shift is easy to miss because it did not arrive all at once. A few years of fast appreciation do not prove a new regime. A local boom can still look temporary. A correction can make it appear that normality has returned. A prosperous city can always claim that higher prices merely reflect success. But once the same pattern repeats across years and then decades — prices rising faster than wages, homes drifting further from building costs, supply responding less strongly than the old model would predict — the problem stops looking cyclical and starts looking structural.

This is where the contrast between a production model and a scarcity model becomes useful.

In the older production model, housing behaves mainly like something that is made. Demand rises, prices rise, and supply expands. Not perfectly, not instantly, and not everywhere in equal measure. But the market still contains a corrective force. Higher prices are not just a burden on buyers; they are also an invitation to produce more homes. Builders respond. Land is brought into use. Neighbourhoods expand. The pressure of demand is translated, at least in part, into physical output.

In the later scarcity model, that relationship weakens. Demand still rises. Prices still rise. But the response on the supply side becomes slower, weaker, and less reliable. The market no longer answers stronger demand mainly by building more. It answers more of it by repricing access to what already exists. Housing begins to behave less like an ordinary good and more like a scarcity asset.

That is what it means to say housing stopped behaving normally.

The older anchors were never absolute, but they mattered. Housing prices remained more closely connected to wages, because ordinary earnings were still more directly related to what ordinary housing cost. Housing prices remained more closely connected to construction costs, because a larger share of housing value still reflected the cost of actually making homes rather than the scarcity premium attached to restricted access. When those anchors weaken badly enough, the entire character of the system changes.

And that appears to be what happened after the postwar era.

A compact proof block makes the break easier to see: [1][5][10][11]

-

Earlier regime Price vs wages: More closely anchored Price vs construction cost: More closely anchored Supply response: Stronger, more normal

-

Later regime Price vs wages: Wider detachment Price vs construction cost: Wider detachment Supply response: Weaker, slower, less reliable

The table is schematic, not exhaustive. Its purpose is to clarify the pattern. In the earlier regime, stronger demand still tended to call forth meaningful new output. In the later regime, stronger demand increasingly called forth larger price movements instead. The crucial point is not that every city changed at the same speed. It is that the governing relationship weakened enough to require a different explanation.

That is why the long-run divergence matters more than any one boom year. If prices rise for a short period and then settle back near wages, build costs, and ordinary supply response, the episode may still be cyclical. But if prices keep outrunning incomes, if the replacement logic of building explains less and less of total housing value, and if supply stops answering demand the way it once did, then a different regime is taking shape.

The exact timing is not identical in every place. Some metropolitan areas hardened earlier than others. Some countries remained more flexible for longer. Some smaller or more permissive regions still behaved more normally even while major constrained cities detached sharply. That unevenness does not weaken the argument. It actually makes it more plausible. Large structural breaks rarely arrive everywhere on the same date. What matters is whether the broad direction changes — and whether the old relationship between demand, price, and supply becomes weak enough to require a new explanation.

That is why the chapter must stay disciplined. It is not here to explain the entire mechanism. It is here to establish that something changed, and that the change runs deeper than a temporary boom.

If housing prices had merely spiked and then returned durably to older relationships with wages and construction costs, this would be a much smaller story. If the apparent break were just the visible expression of one short monetary cycle, it would not deserve a book like this. But that is not what the longer pattern suggests. The later decades increasingly look like a different regime: one in which price growth outruns the practical world of building and the ordinary world of incomes.[1][5][10][11]

That change matters because it changes the kind of remedies people reach for.

If the crisis is mainly cyclical, then cyclical tools look sufficient. Raise rates. Lower rates. Tax speculation. Cool demand. Subsidize entry. Penalize investors. Tinker with mortgage rules. Some of those tools may help at the margin. But if the deeper issue is that housing stopped behaving like a normal production system and began behaving like a scarcity system, then cyclical responses will keep colliding with the same underlying structure. The symptoms may ease for a time. The structure remains.

This chapter therefore makes a limited claim, not a total one. It does not say every housing market detached at the same pace, or that finance and demand conditions do not matter. It says the longer pattern increasingly looks unlike the earlier one, and that the difference is large enough to justify a structural reading.

That is also the falsifier for this chapter. If housing had remained broadly anchored to wages and building costs after 1970, the chapter’s central claim would weaken sharply. If the apparent break were mostly illusory, or merely the temporary effect of one short-lived boom, the anomaly would weaken. If the most constrained markets did not show more severe long-run detachment than more flexible ones, the structural reading would weaken. But the broad pattern points in the other direction: the later period behaves differently enough from the earlier one that a different framework becomes necessary.

That is the real work of this chapter. Not to solve the housing crisis yet, but to change the reader’s time horizon.

Instead of asking:

Why did housing get so crazy in the 2000s?

the reader should now be asking:

What changed earlier that made the later explosion possible?

Once that question becomes unavoidable, the next chapter follows naturally. If housing stopped behaving like a more ordinary production good and began behaving more like a scarcity asset, then the next issue is not yet financial. It is institutional.

What changed in the rules governing land?

That is where the argument has to go next, because the break in housing behavior did not begin with household psychology, moral decline, or even mortgage credit alone. It began earlier, in the way the system decided what land could become housing, when, where, and under what conditions. That is the hinge the next chapter takes up.

Chapter 3 — The 1970s Land-Governance Inflection

The deepest institutional bend began when the land pipeline thickened, slowed, and became more political in the 1970s and after.

Housing crises usually look financial when they first become politically visible. Prices are too high, mortgages are too large, rents are rising, and younger households feel shut out. The instinct is to look for the cause in whatever seems to be pushing hardest at the moment: interest rates, investors, immigration, credit, speculation. But if Chapter 2 is right — if housing stopped behaving like a more ordinary production good before the crisis became fully visible — then the deeper break has to be sought earlier, in the structure that determines how new housing enters the market at all.

That structure is land governance.

The most important shift in this book begins in the 1970s, not because one single law suddenly transformed the country, and not because one party or one leader decided to create scarcity, but because this was the period in which the rules governing land thickened, multiplied, and became more political. What had once been a more expansionary development logic increasingly gave way to a more filtered, procedural, and discretionary one. Land still entered the market. Housing was still built. Growth did not stop. But the path from demand to new supply became slower, narrower, and more contingent.

That is the hinge.

To understand why it matters, it helps to remember the older baseline. Mid-century Canada was not an idyll, and it should not be romanticized. But it was, in material terms, more builder-oriented. Population growth was more readily met by expansion. Suburbs were serviced. Land was converted. Infrastructure and housing were added at large scale. The governing assumption of that world was not that every proposal should proceed automatically, but that growth was normal and provision was part of ordinary state and market activity. In housing, that meant the system was more prepared to respond to rising demand by making more places to live.

The 1970s did not abolish that world overnight. What changed was the accumulation of new filters between land and housing. Planning systems thickened. Zoning became more restrictive and more detailed. Review layers expanded.[7][9] Hearings and discretionary approvals became more central. Agricultural land protections, environmental review processes, neighbourhood objections, servicing constraints, and procedural veto points began to carry more weight. Each change could be defended in isolation. Some were meant to prevent real harms. Some reflected legitimate concerns about sprawl, environmental damage, infrastructure strain, or loss of local control. The point is not that all restraint is irrational. The point is that, taken together, these changes altered the institutional character of the land pipeline.

Land no longer entered the housing system in the same way.[7][9]

A compact historical anchor makes the bend clearer: [7][9][10]

-

Earlier expansion model Governing tendency: Provision first Land pipeline character: More direct, more expansionary Typical effect: Demand translated more readily into land release and housing

-

1968–1985 hinge zone Governing tendency: Cumulative thickening Land pipeline character: More review, more conditions, more discretion Typical effect: Slower, narrower, more contested conversion of land into housing

-

Later scarcity regime Governing tendency: Managed access Land pipeline character: More political, more filtered, more approval-dependent Typical effect: Growing difficulty turning demand into timely new supply

This is not a claim that every jurisdiction moved at the same speed or by the same route. It is a way of stating the structural pattern. The important change was cumulative. More procedural steps. More approval layers. More zoning complexity. More chances for delay, downsizing, challenge, conditioning, or refusal. A system that had once been more oriented toward release and provision became more oriented toward supervision and control.

That is why the period from roughly 1968 to 1985 matters so much in the architecture of this book. It is the hinge zone in which the older, more expansionary model gives way to a new one. Again, this was not one-law causation. It was cumulative thickening. More review. More zoning complexity. More political discretion. More points at which a project could be delayed, resized, challenged, conditioned, or stopped.

Concrete examples help clarify what “thickening” means in practice. A housing project that might once have moved through a relatively straightforward land-conversion and servicing path increasingly had to pass through rezoning battles, public hearings, environmental assessments, traffic and design review, infrastructure conditions, growth-boundary or farmland constraints, and more discretionary municipal approval. None of these devices needed to prohibit growth in absolute terms to change the system. They only needed to make growth slower, riskier, less predictable, and more political.

That distinction is subtle enough to be missed in real time. A country can still think of itself as one that builds while gradually making building harder. Technical capacity can remain while institutional throughput declines. Developers can still exist, cranes can still appear, subdivisions can still be approved, and yet the overall governing pattern can shift decisively. That is exactly what makes the 1970s inflection so important. The country did not suddenly forget how to build. It changed the terms under which building could occur.

And once that happens, scarcity no longer needs to be understood mainly as physical shortage. It becomes increasingly institutional.

This is the crucial point of Chapter 3. The problem was not that Canada literally ran out of land. It was that the amount of land that could legally, procedurally, and politically become housing was now passing through a narrower system. The relevant scarcity was not raw geographic acreage. It was politically available land.[7][9][10] That distinction becomes fully economic in the next chapter. Here it remains institutional: land release became slower, more filtered, and more contestable.

That is also why this chapter must stay calm and precise. It should not overclaim motive when process explains enough. One does not need a conspiracy theory to explain what happened. It is enough to see that the governing philosophy of land use changed. Earlier systems tended to assume that growth should be accommodated unless strong reasons blocked it. Later systems increasingly assumed that growth should be negotiated, reviewed, and conditioned through a much thicker process. That altered the housing system even before the full consequences were obvious.

And the consequences were not instantly obvious. A thicker planning regime does not produce crisis on day one. It first produces slower release, more delay, more uncertainty, more friction, and more dependence on approvals. If other conditions remain calm, the system can appear manageable. But once demand rises harder — through population growth, income growth, urban concentration, or later credit expansion — the institutional bend begins to matter much more. The market can only respond through the channels the land system permits. If those channels have narrowed, price pressure will eventually begin to outrun the old corrective logic.

That is why starting the story in the 2000s gets the whole chronology wrong. By the time finance, speculation, and visible affordability crisis dominated public attention, the deeper institutional change had already taken place. The land system had been altered first. The later crisis piled itself on top of that altered structure.

This chapter also needs a clear limit. It is not yet the chapter that explains supply elasticity in full. It is not the chapter that compares flexible and constrained markets in detail. It is not the finance chapter. It is not the demographic chapter. Its task is narrower and more foundational: to show that the rules governing how land becomes housing changed decisively enough in the 1970s and after to create a different kind of housing system.

That claim is falsifiable. If land release had remained broadly as responsive, simple, and administratively light as it had been in the earlier model, then the argument of this chapter would weaken sharply. If the 1968–1985 period did not show a meaningful thickening of planning, approval, zoning, and review systems, the hinge would weaken. If later housing stress appeared without any prior institutional constriction of the land pipeline, then a different deep explanation would be needed. But that is not the pattern that keeps emerging. The more persuasive pattern is one of cumulative procedural thickening, growing discretion, and a land pipeline that became progressively more political over time.

That is the institutional bend on which the whole book turns.

The crucial change was not simply that more rules existed. It was that land entered the housing system through a slower, more discretionary, and more political process. Once that happened, the next question was no longer historical but economic: how does a housing market behave when supply can no longer respond normally to rising demand?

That is the mechanism of land gatekeeping, and it is the work of the next chapter.

Chapter 4 — The Gatekeeping of Land

When land supply is gated, rising demand is translated less into new housing and more into higher prices.

A housing market can look like a demand problem even when its real bottleneck lies somewhere else.

That is one of the reasons housing debates become so confused. Prices rise, rents jump, buyers panic, and public attention rushes toward whatever seems to be pushing from the demand side: immigration, investors, low interest rates, speculation, urban concentration, household formation. All of those forces can matter. But a housing system is not defined only by how much demand it receives. It is also defined by what it does when that demand arrives.

Does it build?

Or does it reprice?

That is the question at the center of land gatekeeping.

Chapter 3 showed the institutional bend: land entered the housing system through a slower, more filtered, and more political process. This chapter explains what that change does economically. Once land supply becomes politically constrained, the market loses part of its ability to respond normally to higher demand. Rising prices no longer call forth enough new housing. They increasingly call forth competition for access to a scarce and tightly controlled supply.

That is the mechanism.

The key concept is supply elasticity.[8] In plain language, supply elasticity means how strongly and how quickly new housing appears when prices rise. In an elastic system, higher prices encourage more building, and the system is capable of responding.[8][10][11] Land is released, permissions are granted, projects move, and additional housing enters the market fast enough to absorb at least part of the pressure. Prices may still rise, but the rise is moderated by output.

In an inelastic system, the same demand shock produces a different result.[8][10][11] Prices rise, but supply responds weakly, slowly, or unpredictably. Builders may want to build more, but the path from proposal to completion is blocked by delay, uncertainty, zoning limits, political discretion, servicing constraints, hearings, or outright refusal. In that case, higher prices do not trigger enough additional homes. They trigger harder competition for what already exists.

That is why land gatekeeping matters so much. It changes the answer the housing system gives when demand increases.

In the older, more production-oriented model, the answer was more often: build more.

In the scarcity-oriented model, the answer becomes more often: charge more.

This is where a second distinction becomes essential: the difference between total land and politically available land. Canada, in the abstract, is not short of land. That is obvious enough to become misleading. The relevant question is not how much land exists on a map. The relevant question is how much land can legally, procedurally, financially, and practically become housing where demand is concentrated. Once that channel narrows, national abundance matters much less than institutional access.

That is why the most expensive cities can exist in physically large countries. The scarcity is not simply natural. It is institutional.[7][8][10] It is created by the width of the gate through which land must pass before it can become housing.

A compact comparison makes the mechanism clearer: [5][6][8][10][11]

-

More flexible / elastic market What higher demand does: Signals builders to expand output Typical supply response: Faster land release, approvals, and construction Typical price effect: Some price rise, but more pressure absorbed through new housing

-

More constrained / inelastic market What higher demand does: Intensifies competition for scarce permissions and sites Typical supply response: Slower, weaker, less predictable output response Typical price effect: Larger and more persistent price escalation

Once that point is visible, the price logic becomes easier to understand. If a city grows, incomes rise, and more households want access to the same urban region, then prices will move upward. But what happens next depends on elasticity. In a more flexible system, those higher prices draw out more supply. Developers assemble sites, zoning permits more housing, approvals are more predictable, and the increase in demand gets translated partly into more homes. In a constrained system, those same higher prices do not unlock enough new supply. They simply increase the value of scarce permissions and scarce sites. Demand is still there. Money is still there. But the system cannot widen fast enough. So the extra pressure moves into prices.

That is why the same city can look prosperous and dysfunctional at the same time.

On the surface, high prices seem to signal success. People want to live there. Capital is flowing in. Owners appear richer. But if those rising prices are not matched by an adequate increase in housing output, then the prosperity is telling a deeper story. It is not just that the city is desirable. It is that access to it is being rationed through price.

A simple concrete example makes the mechanism clearer. Imagine a piece of land near an established urban area that could, in physical terms, hold mid-rise housing. In a more flexible system, stronger demand makes that project easier to justify and easier to execute. The land can be developed, units can be added, and some of the price pressure is absorbed through new supply. In a gated system, that same site may require rezoning, public hearings, neighbourhood consultation, traffic review, design revision, infrastructure conditions, environmental assessment, density negotiation, and political approval before it can move. The site may still eventually be built. But the path is slower, riskier, and more uncertain. In that environment, permission itself becomes scarce and valuable.

The system is no longer just selling housing. It is selling access to permission.

That is one reason housing prices can detach so sharply from building costs. The structure still matters, but the site and the rights attached to it matter more. A modest or aging house can become extraordinarily expensive not because the house itself has become extraordinary, but because it sits on land whose redevelopment or continued use is protected by a scarcity system. The physical object may be ordinary. The controlled access is not.

A second compact proof block helps show the difference: [5][10][11]

-

Value component: Structure value In a more normal production system: Larger share of total value reflects actual build cost and quality In a scarcity-gated system: Still matters, but weaker as a driver of price escalation

-

Value component: Land / permission value In a more normal production system: Important, but more constrained by ability to add comparable supply In a scarcity-gated system: Expands sharply as access becomes scarce and approval-dependent

-

Value component: Price movement under pressure In a more normal production system: More output, moderated repricing In a scarcity-gated system: Less output, stronger repricing

This is also why constrained and flexible markets behave differently under pressure. In more flexible systems, demand growth produces more supply response. In more constrained systems, the same demand growth produces a larger price response.[5][8][10][11] Geography, labour costs, and local conditions still matter. Building a tower downtown is not the same as expanding low-rise housing at the edge. Some places are genuinely harder to build in than others. But those factors alone do not explain the whole pattern. The more important issue is whether the system can expand enough when it needs to. In the markets where housing becomes most detached from ordinary incomes and building costs, the recurring answer is that it cannot.

That is the heart of the chapter: land scarcity in the modern housing crisis is often not pure physical scarcity. It is scarcity produced and reinforced through governance.[7][8][10]

That does not mean all land-use regulation is irrational. Some restraint is necessary. Cities cannot function without coordination. Infrastructure has limits. Environmental concerns can be real. Not every proposal should be approved automatically. But that caveat does not change the mechanism. The problem begins when the cumulative effect of land governance is to suppress normal supply response so heavily that rising demand is translated mainly into higher prices rather than additional housing.

This chapter also has a clear interpretation limit. It does not claim that every expensive market is explained only by regulation, or that geography, labour shortages, infrastructure limits, or local building conditions do not matter. It claims something narrower and stronger: when the land pipeline becomes sufficiently gated, those pressures operate inside a system that is already less capable of converting demand into supply. The result is more repricing and less provision than a more elastic system would produce.

And that claim is falsifiable. If highly constrained systems still produced supply responses comparable to flexible ones, this explanation would weaken. If the most expensive markets stayed close to construction cost while adding plenty of housing under pressure, the explanation would weaken. If land governance had become more elaborate without materially affecting the quantity response of supply, the explanation would weaken. But the pattern that keeps emerging points in the opposite direction: where land becomes harder to release and housing harder to approve, the market answers demand less with building and more with repricing.

That is why Chapter 4 belongs at the center of the book. It is the machine chapter. Chapter 3 showed the institutional bend. Chapter 4 shows what that bend does. Once the gate narrows, every later force becomes more inflationary than it otherwise would have been. Demand becomes more destabilizing. Population growth becomes harder to absorb. Speculation becomes more damaging. And mortgage credit, when it arrives in force, no longer solves the shortage. It collides with the bottleneck and magnifies it.

That is the problem the next chapter takes up.

Chapter 5 — Credit Turned Scarcity into Asset Inflation

Credit did not create the bottleneck; it amplified an already constrained housing system.

A blocked system does not stop responding when more money enters it. It responds differently.

That is one of the central facts of modern housing finance, and it is where a great deal of public explanation goes wrong. People see housing prices surge, see mortgage debt expand, and conclude that cheap credit must have caused the entire crisis. The instinct is understandable. Borrowing costs fell. Mortgage terms lengthened. Leverage increased. Insurance widened access to debt. Securitization deepened the funding base behind home lending. If the story begins in the 1990s or 2000s, finance can easily appear to be the main event.

But it is not the first break in the chain.

The earlier chapters have already established something more fundamental. Housing stopped behaving normally before the full visible crisis. The 1970s and after brought a decisive change in land governance. The supply side became slower, narrower, and more political. By the time mortgage credit expanded dramatically, it was not entering a wide-open production system. It was entering a bottleneck.[5][11]

That sequencing matters.

If the land pipeline had remained broadly responsive, easier credit would still have pushed prices upward to some extent, but it also would have helped finance more building. More households with more borrowing power would have created stronger signals for developers, and more of that demand would have been translated into additional homes. But once the land system had already become less elastic, the effect of credit changed. More money no longer produced enough additional supply. It produced harder competition for access to a constrained supply.

That is the mechanism of amplification.

Chapter 4 explained why rising demand in an inelastic land system produces price escalation more reliably than quantity expansion. Chapter 5 shows what happens when that same inelastic system is struck by a major increase in purchasing power. The answer is straightforward. Credit does not remove the bottleneck. It pushes more financial force against it.[11][12][14][15] Instead of solving scarcity, it capitalizes scarcity into higher land values, higher home prices, and larger balance-sheet gains for those who already own access.

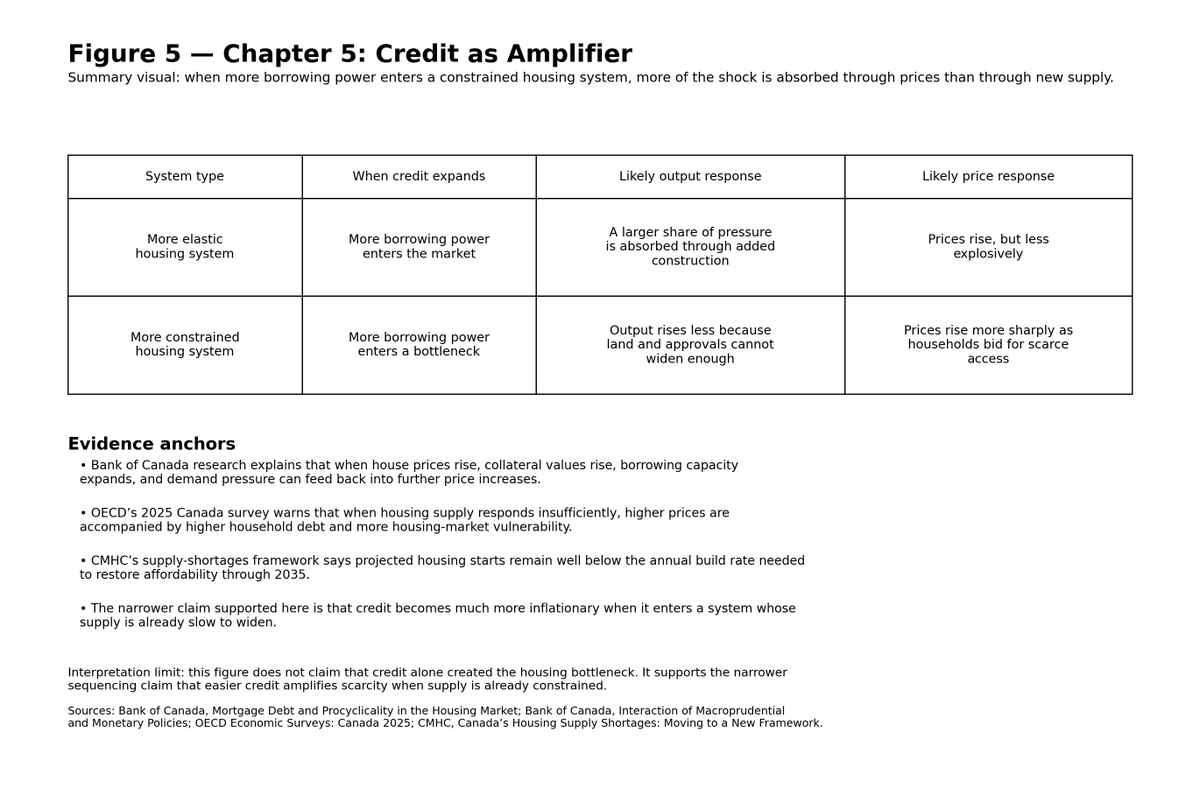

This is why the same amount of credit does not have the same effect everywhere.[11][12][14]

In a more elastic system, easier financing still matters, but part of its pressure is absorbed through output. Builders can respond. Land can enter use more readily. Projects move faster. Supply rises more meaningfully. In a constrained system, that response is weaker. Households borrow more, but housing supply cannot scale enough to meet that expanded purchasing power. The result is that the extra money is translated less into more homes and more into higher bids for existing homes and sites.

That is the point at which scarcity becomes financially amplified.

A compact comparison helps show the distinction: [11][12][13][14]

-

System type: More elastic housing system When credit expands: More borrowing power enters the market Likely output response: A larger share of pressure is absorbed through added construction Likely price response: Prices rise, but less explosively

-

System type: More constrained housing system When credit expands: More borrowing power enters a bottleneck Likely output response: Output rises less because land and approvals cannot widen enough Likely price response: Prices rise more sharply as households bid for scarce access

The underlying finance story is familiar enough. Over time, households gained access to larger mortgages through a combination of lower rates, longer amortization periods, more permissive leverage norms, securitized mortgage funding, and government-backed insurance structures that widened access to debt. None of those changes is inherently pathological in isolation. Mortgage finance can support stable ownership and normal development. Credit is not the villain simply because it exists. The important question is what kind of system that credit is entering.

That is why the order of explanation has to remain clear. Credit is the amplifier, not the root shift.[11][12][14]

This distinction is more important than it looks. If one mistakes credit for the original cause, then the whole crisis begins to look like a purely monetary event. But the stronger reading is that finance became so destructive because it hit a housing system whose land supply had already been made less responsive. The credit shock did not create scarcity from nothing. It accelerated the repricing effects of scarcity that were already structurally in place.[5][11][12][14]

A simple model makes the point. Housing outcomes depend heavily on the interaction of four things: demand, credit, supply elasticity, and land constraints. When demand rises and credit rises in a system with relatively high supply elasticity, more housing tends to follow and some of the pressure is absorbed physically. When demand rises and credit rises in a system with low elasticity and strong land constraints, price rises faster because output cannot respond adequately. The same financial impulse becomes more inflationary when it strikes a narrower housing pipeline.

That is why a pure credit story is inadequate.

A second compact proof block sharpens the sequence: [11][12][13][14][15]

-

Step: 1. Demand strengthens More normal production system: Prices rise and signal expansion Scarcity-constrained system: Prices rise and intensify access pressure

-

Step: 2. Credit expands More normal production system: Developers and households both gain room to act Scarcity-constrained system: Households gain bidding power faster than supply gains room to expand

-

Step: 3. Supply response More normal production system: More output absorbs part of the shock Scarcity-constrained system: Weak output response leaves the shock concentrated in prices

-

Step: 4. Result More normal production system: Some inflation, but more building Scarcity-constrained system: Asset inflation layered on top of scarcity

Canada is not the only place with mortgage finance. Fast-growing Texas metros have had credit, population growth, and economic expansion. Japan has had mortgage finance and dense urban demand. Yet price behaviour differs sharply across systems. The crucial difference is not that credit exists in one place and not another. The difference is how much of the resulting pressure gets converted into new housing and how much gets converted into price. Flexible systems absorb more through output. Constrained systems absorb more through land appreciation.

This is also why the crisis often appears to gather force gradually and then become suddenly obvious. The bottleneck forms first. Then mortgage finance expands. Then other pressures intensify — population growth, investor activity, urban concentration, low-rate conditions. The public experiences the later explosion and assumes the most visible recent force must be the cause. But the deeper chronology runs the other way. The land system bends first. Finance then turns that bend into a much steeper price regime.

Once that happens, housing changes character.

That full social and economic meaning belongs more fully to Chapter 7, but its causal foundation appears here. A home in a financially amplified scarcity system is no longer just shelter with some investment value attached. It becomes a leveraged claim on constrained access. Appreciation becomes central to expectations. Rising value becomes normal rather than exceptional. Ownership begins to look less like secure occupancy and more like entry into the dominant escalator of household wealth.

That shift matters because it generates its own loop. More borrowing power raises prices. Higher prices justify larger loans. Larger loans normalize heavier leverage. Heavier leverage makes appreciation more important to household stability. In a system that could expand supply quickly, that loop would still exist but would be moderated. In a blocked system, it intensifies the repricing of existing access.

This is the narrower and stronger way to state the chapter’s capital-allocation concern. The problem is not that every dollar associated with housing would otherwise have gone into some ideal productive use. That claim would be too sweeping. The stronger point is that a society in which wealth is increasingly accumulated through the repricing of already scarce land is different from one in which wealth is accumulated more heavily through creating new assets and capacity. Housing inflation can make a country appear richer on paper while leaving the underlying production of new shelter far behind the growth of nominal values.

This chapter also has a clear interpretation limit. It does not claim that credit alone explains the crisis, or that monetary conditions are unimportant. It claims something narrower and stronger: once the land pipeline has already been constrained, credit becomes much more inflationary than it would be in a more responsive housing system. The damage comes from the interaction of finance with scarcity, not from finance in isolation.

This chapter is also falsifiable. If large credit expansion in highly constrained markets did not produce stronger price escalation than in more flexible markets, the amplifier claim would weaken. If mortgage expansion in constrained systems routinely generated enough new supply to keep prices close to construction cost, the claim would weaken. If the timeline were reversed — if major mortgage expansion clearly came before the land bottleneck — the sequencing argument would weaken. But the broader pattern points the other way. The structural constriction came first; the financial amplification came later; the visible crisis became much harsher because both were now operating inside the same system.

That is why mortgage credit must be treated neither as the whole story nor as a side issue. It is not the first cause of the housing crisis, but it is one of the main reasons the crisis became so extreme. Without the land bottleneck, finance would have been less destructive. Without the credit expansion, the bottleneck would still have mattered, but its repricing effects would likely have been slower and less explosive. The modern housing system emerged from the interaction of both.

And once that interaction matures, the next development follows naturally. Rising values no longer benefit owners merely by accident. They begin to create a class of insiders — and a set of governments — whose stability becomes tied to the continuation of the appreciation regime. The system no longer just produces scarcity. It begins to defend it.

That is the problem the next chapter takes up.

Chapter 6 — Homeowner Politics and the Self-Reinforcing System

Once scarcity generates gains for insiders and dependence for governments, the system begins to defend itself.

The hardest systems to change are usually the ones that reward the people already inside them.

That is the political fact at the center of the housing crisis. By the time scarcity becomes painful enough for outsiders to recognize it as a crisis, it has often already become valuable enough for insiders to defend it. This is why housing is not just an economic problem or a planning problem. It is also a problem of political reinforcement. Once rising home values become central to household balance sheets, neighbourhood expectations, municipal revenues, and public assumptions about stability, scarcity is no longer just an accidental outcome of bad design.[12][13][14] It becomes a regime with defenders.

That does not mean a conspiracy is required. It means incentives are enough.

The earlier chapters have already established the sequence. Housing stopped behaving normally. Land release became more political. Supply elasticity weakened. Credit later amplified the resulting scarcity. Prices then rose far more sharply than they would have in a more responsive system. Chapter 6 asks the next necessary question: once that price regime is in place, why doesn’t the system correct itself?

The answer begins with homeowners.

For households that already own property, rising housing values can feel like security, prudence rewarded, or simply normal economic life. A house is not just a place to live. It is often the largest asset a family owns. When its value rises, the household feels safer. Net worth grows. Borrowing capacity improves. Future options seem to expand. None of this is irrational. People respond to incentives in the world they actually inhabit. If a family’s main store of wealth is tied to its home, then any change that appears likely to weaken that value will be treated not as an abstract policy adjustment, but as a threat.

This is one of the reasons housing politics becomes so difficult. The same change that looks like overdue relief to an outsider can look like loss to an insider.

That does not mean every homeowner thinks the same way, votes the same way, or opposes all development. Many owners support more housing. Many understand that the system has become exclusionary. Many have children who are themselves being shut out. The point is structural, not moral. A system in which large numbers of households have become dependent on appreciation creates a powerful background incentive to resist anything that seems likely to reduce scarcity too quickly.

That incentive becomes especially visible at the local level.

When new housing is proposed, opposition rarely presents itself as naked asset defense. It appears in more respectable forms: traffic concerns, neighbourhood character, school pressure, shadows, parking, trees, infrastructure strain, consultation rights, planning process, quality-of-life language. Some of those concerns may be genuine in individual cases. But the larger pattern is difficult to miss. Existing residents, especially in high-value areas, are often positioned to slow, resize, condition, or stop additions to the local housing stock.[7][14] The power may be informal or formal, electoral or procedural, but the effect is the same. Scarcity is defended through local veto points.

A compact political-economy sketch makes the loop visible:[7][12][13][14]

-

Mechanism: Rising home values Immediate effect: Owners become more balance-sheet sensitive Regime effect: Resistance to rapid supply expansion strengthens

-

Mechanism: Local veto points Immediate effect: Projects can be delayed, reduced, or blocked Regime effect: Supply remains politically fragile

-

Mechanism: Fiscal dependence on high property values Immediate effect: Governments fear sharp downward adjustment Regime effect: Reform becomes more cautious and incremental

That is why the housing system so often feels irrational from the outside. A city can declare a housing shortage and still allow neighbourhood-scale resistance to repeatedly block the kinds of additions that would ease it. It can describe affordability as a central problem while preserving the land-use and approval structures that keep supply politically fragile. The contradiction is not accidental. It reflects the fact that the people already inside the system often possess both the strongest incentives and the greatest leverage to preserve its advantages.

This is the scarcity loop.

Scarcity raises values. Higher values make existing owners more sensitive to change. Greater sensitivity strengthens resistance to additional supply. Resistance keeps supply constrained. Constrained supply preserves scarcity. And preserved scarcity supports further price escalation. The system does not merely fail to correct itself. It begins to reproduce the conditions of its own persistence.

But homeowners are not the only actors adapting to the regime. Governments adapt too.

Municipalities and other public bodies increasingly operate inside an environment in which property values matter not only socially but fiscally.[12][13][14] Rising assessments strengthen tax bases. Development charges, transfer taxes, and other housing-linked revenues become politically and budgetarily significant. Governments begin speaking the language of affordability while simultaneously relying on the continuation of a high-value property regime. This produces a deep ambivalence. Public institutions may want relief from the crisis, but they are also entangled with the very asset inflation that defines it.

That is the fiscal dependence loop.

A government that depends heavily, directly or indirectly, on high property values is not a neutral referee standing outside the housing system. It becomes one more actor adapting to scarcity. The dependence need not be total to matter. It only has to be strong enough to make large downward adjustment politically frightening. A regime can be harmful overall while still being stabilizing for the actors already organized inside it.

A second compact proof block clarifies the reinforcing structure: [7][12][13][14]

-

Actor: Incumbent homeowners What scarcity provides: Appreciation, collateral, perceived security Why reform becomes harder: Policies that threaten rapid repricing feel personally risky

-

Actor: Local organized residents What scarcity provides: Procedural leverage over neighborhood change Why reform becomes harder: Additional housing can be opposed project by project

-

Actor: Municipal governments What scarcity provides: Stronger assessments and housing-linked revenues Why reform becomes harder: Large value declines appear fiscally dangerous

This is part of why reform so often looks timid relative to the size of the problem. The issue is not simply that policymakers fail to understand the housing crisis. It is that they operate within a structure where too many forms of household security, local political stability, and public finance have become tied to continued appreciation. The regime may be exclusionary, but it is also familiar. It may be distortionary, but it is also deeply embedded.

That is what makes the system self-reinforcing.

And it is important, again, not to moralize too quickly. It is easy to turn this into a story of villains and victims alone. There are victims, certainly.

Younger households, renters, and later entrants bear the costs most heavily. There are also actors who benefit. But the strongest explanation is not that a malicious class simply chose to starve the country of housing. The stronger explanation is that once scarcity, appreciation, and balance-sheet dependence became intertwined, a wide range of normal, defensible, even ordinary behaviors began pushing in the same direction. Caution, self-interest, local control, fiscal dependence, political fear, and administrative inertia all began reinforcing a system that no longer served newcomers well.

That is why housing reform is harder than it first appears. It is not only a technical problem of zoning text, approvals, or financing structures, though it includes all of those. It is also a problem of dislodging a political economy that has learned to live off scarcity. A regime that produces gains for insiders, stability for local incumbents, and revenue for governments will not dissolve simply because its exclusions become obvious.

This chapter also has an interpretation limit. It does not claim that every homeowner is anti-housing, that every local objection is fraudulent, or that governments consciously prefer exclusion as such. It claims something narrower and stronger: once appreciation becomes central to household security and public finance, the political system acquires built-in reasons to move cautiously, defend existing advantages, and preserve scarcity longer than the social interest would justify.

This chapter is also falsifiable. If rising home values did not correlate with stronger local resistance to added supply, the political reinforcement argument would weaken. If governments were largely indifferent to the fiscal consequences of housing appreciation, the fiscal loop would weaken. If scarcity intensified without producing insider incentives to preserve it, this chapter would weaken. But the broad pattern points in the other direction: once appreciation becomes central, opposition hardens, caution multiplies, and reform becomes politically more difficult than the scale of the crisis would otherwise suggest.

That is why scarcity has to be understood not only as a market outcome, but as a defended equilibrium.

And once that equilibrium is in place, housing begins to change category. It is no longer just expensive shelter inside a bad system. It becomes a central object of wealth, security, and expectation. That broader change in the social role of housing is the subject of the next chapter.

Chapter 7 — From Shelter to Financial Asset

In a scarcity regime, housing becomes central not just to shelter but to balance sheets, security, and intergenerational advantage.

A society changes when homes are valued less for what they do and more for what they are expected to become worth.

That is not the whole story of modern housing, but it is one of its deepest social consequences. Homes do not cease to be shelter. They still protect people from weather, give families privacy, anchor neighbourhoods, and make daily life possible. But in a scarcity regime that has already been financially amplified and politically defended, homes cease to be understood mainly as places to live. They begin to function increasingly as stores of wealth, vehicles of security, and instruments of intergenerational advantage.

That is the category shift this chapter is about.

Earlier chapters showed how the system got here. Housing stopped behaving like a more ordinary production good. Land release became more political. Supply elasticity weakened. Credit then drove more purchasing power into a bottlenecked system. Homeowners, local politics, and governments adapted themselves to rising values. Chapter 7 asks what this does to the social and economic meaning of homeownership itself.

The answer is that housing becomes more central to life chances than shelter alone can explain.

In a healthy housing system, buying a home can still be financially important, but the basic meaning of the home remains stable. It is first a place to live, then perhaps a useful form of savings. In the scarcity regime, that order begins to reverse. The home is still shelter, but it is increasingly treated as the primary household asset, the main collateral base, the central retirement pillar, and the most important mechanism through which families secure long-term stability.[3][4][12][13] What matters is no longer just that a home provides occupancy. What matters is that it participates in a rising asset regime.

That difference changes behaviour.

A household that sees housing mainly as shelter asks one kind of question: Can we find a decent place we can afford to live in? A household that sees housing as the dominant escalator of wealth asks a different one: How do we get in before prices move even further away from us? The emotional atmosphere shifts from ordinary purchase to strategic entry. Timing becomes more important. Family help becomes more decisive. Missing the market by a few years can begin to feel like missing the main track of middle-class security altogether.

This is one reason the housing crisis becomes so psychologically intense even before it becomes demographically visible. The issue is not simply that prices are high. It is that ownership increasingly appears to determine who gets access to the strongest balance-sheet gains and who remains outside them.[3][4][12][13] In such a system, a home does not feel like one asset among many. It begins to feel like the asset.

That is what makes housing different from most consumer goods. Very few people panic about buying a refrigerator before it runs away from them. Very few families reorganize long-term life plans around whether they entered the dishwasher market in time. Housing in a scarcity regime becomes different because it is not merely consumed. It is accumulated, leveraged, inherited, and defended.

This is where balance-sheet centrality matters. As home values rise, ownership stops being only a matter of secure occupancy and becomes a matter of net worth formation.[3][4][12][13] Equity can be borrowed against. Appreciation can be counted on, or at least hoped for, as part of retirement planning. Parents begin to think about homes not just as where they live, but as what they may pass on. A family already inside the market becomes differently situated from a family still outside it, not merely because one has shelter and the other rents, but because one now participates in the country’s dominant appreciation machine while the other does not.

A compact proof sketch makes the shift visible:[3][4][12][13]

-

Housing role: Primary meaning More normal housing system: Shelter first, savings second Scarcity-financialized housing system: Asset first, shelter still present

-

Housing role: Household strategy More normal housing system: Buy when affordable for occupancy Scarcity-financialized housing system: Enter early to capture appreciation

-

Housing role: Wealth formation More normal housing system: More tied to earnings and saving Scarcity-financialized housing system: More tied to prior ownership and timing

-

Housing role: Family advantage More normal housing system: Helpful but not decisive Scarcity-financialized housing system: Down-payment help and inherited equity become far more important

That shift changes the meaning of inequality.

The older and simpler forms of housing inequality were already serious: some households owned and some rented; some locations were desirable and others less so; some people entered more easily than others. But the scarcity regime deepens those differences by linking housing more tightly to wealth accumulation. A homeowner in a rapidly appreciating market is not just avoiding rent. That person is often receiving large capital gains that derive less from improving the home itself than from owning scarce access early enough. The late entrant, by contrast, is not merely paying more. That person is often paying into a system in which the major wealth effects have already accrued to someone else.

This is why intergenerational position becomes so important.

Once housing becomes a major wealth vehicle, the difference between families who already own and families who do not begins to widen in new ways. Parents with housing equity can help with down payments. Earlier owners can refinance, borrow, or transfer value. Younger adults with family property behind them enter the market differently from those relying on earnings alone. Timing begins to matter almost as much as effort. The difference between being born into an owning household and into a non-owning one becomes more consequential. A system that once looked merely expensive starts to behave more like one that allocates security through inherited advantage.

A second proof block clarifies the intergenerational channel:

-

Channel: Down payment Insider family: Can often be assisted by parental equity Outsider family: Must rely more heavily on wages and saving

-

Channel: Market entry timing Insider family: Earlier entry more feasible Outsider family: Later entry more likely

-

Channel: Balance-sheet growth Insider family: Appreciation compounds family advantage Outsider family: Rent and higher entry prices delay accumulation

-

Channel: Security transfer Insider family: Housing wealth can be passed forward Outsider family: Little or no housing asset base to transfer

That does not mean the country becomes a feudal society overnight. It means the logic of housing shifts. Entry is no longer governed mainly by ordinary earnings and ordinary purchase timing. It becomes more dependent on prior asset ownership, family assistance, and being inside the appreciation cycle early enough.

That is the narrower and stronger meaning of the phrase from shelter to financial asset.

It does not mean homes stop sheltering people. It does not mean every homeowner becomes a speculator. It does not mean no one cares about neighbourhood, beauty, stability, or family life.

It means the dominant social meaning of ownership changes. A home increasingly matters because of what it protects on the balance sheet and what it may become worth later, not only because of what it provides now.

This also changes the character of national wealth. A society organized around building new assets differs from one organized around repricing access to existing ones. The claim here should be stated carefully. It is too simplistic to say that every dollar of housing wealth crowds out some other productive investment one for one. But it is still true that an economy in which security and wealth are increasingly tied to existing land is different from one in which prosperity is generated more heavily by producing new capacity. In the first kind of system, more value is created by getting into the right asset early enough. In the second, more value is created by adding to what the society can actually build and provide.

That difference is not yet the full civilizational interpretation of the book. That belongs later. Here it remains concrete and social. A repricing regime produces one kind of household life. A building regime produces another.

In a repricing regime, families watch the market the way previous generations watched wages. Security becomes more asset-dependent. The housing ladder becomes steeper. Earlier entry matters more. Family transfer matters more. The line between shelter and wealth becomes harder to separate. What looks like a housing market is increasingly also a sorting system for life chances.

This chapter also has an interpretation limit. It does not claim that housing is the only important household asset, that all inequality now flows through real estate, or that every ownership market functions the same way. It claims something narrower and stronger: in the most distorted and supply-constrained markets, housing has become too central to balance sheets, family strategy, and intergenerational transfer to be understood merely as shelter with a modest savings function attached.

This chapter is also falsifiable. If housing appreciation had not become central to household balance sheets, retirement expectations, and intergenerational assistance, then the category-shift claim would weaken. If ownership in the major constrained markets still functioned mainly as straightforward shelter rather than as a dominant vehicle of wealth formation, the claim would weaken. If later entrants could access ordinary homeownership on ordinary earnings without heavy dependence on prior family assets or extreme leverage, the claim would weaken. But the broader pattern points the other way: in the most distorted markets, housing has become too important to be understood merely as shelter.

And once that happens, the next consequence follows naturally. If access to stable housing increasingly governs access to adult security, then housing begins to shape not just wealth, but timing — when people leave home, when they form households, when they partner, when they have children, and how securely they can imagine the future.

That is the subject of the next chapter.

The claim is narrower and stronger: when a society’s institutions cease mainly to coordinate and guide building, and instead increasingly slow, filter, ration, and politicize it, scarcity becomes the default output of the system.

That is the turn this chapter is naming.

In a builder-oriented order, institutions are used to make provision possible.

In an administrative-scarcity order, institutions are increasingly used in ways that make provision more difficult, delayed, discretionary, and uncertain.

The economic consequences of that shift were already shown earlier in the book. Land supply becomes less elastic. Prices rise faster than output. Credit becomes more inflationary. Ownership becomes more valuable. Exclusion hardens. What Chapter 9 adds is a broader reading of what those outcomes suggest. A society that repeatedly answers pressure with repricing rather than provision is not merely making isolated policy mistakes. It may be expressing a different governing instinct.

That is why housing is so revealing. It is not a niche sector. It is ordinary enough, central enough, and measurable enough to expose the larger pattern. If a society struggles to provide ordinary housing in response to ordinary demand, then something important has shifted in its relation to building itself.

That does not prove a grand total theory of Canada. It does, however, justify a serious interpretation: housing is the clearest measurable surface on which a broader transition from builder logic to managed scarcity can be observed.

The three layers help keep this disciplined.

At the civilizational layer, the governing instinct shifts from building additional capacity toward managing and filtering access.

At the institutional layer, this appears as thicker approval systems, more veto points, slower throughput, longer timelines, and a more political land pipeline.

At the economic layer, the measurable result is constrained supply, higher land premia, asset inflation, and housing that behaves less like a mass-produced good and more like a protected positional asset.

A compact summary shows the interpretive chain:

-

Layer: Civilizational Builder-oriented pattern: Pressure answered with added capacity Administrative-scarcity pattern: Pressure answered with managed access

-

Layer: Institutional Builder-oriented pattern: Rules coordinate and enable provision Administrative-scarcity pattern: Rules slow, filter, and politicize provision

-

Layer: Economic Builder-oriented pattern: More output, more responsiveness, weaker land premia Administrative-scarcity pattern: Less responsiveness, higher land premia, more asset inflation

That layering matters because it prevents two equal mistakes. The first mistake is to treat housing as a purely technical policy problem with no deeper meaning. The second is to leap from housing directly into sweeping civilizational despair. The stronger position lies between them. Housing is not everything, but it is enough. It is enough to show that something larger may have changed in how the society builds, governs, and allocates.

This is also where the chapter must show restraint. It should not wander into elite motive stories, party grievance, or abstract cultural lament. It should not pretend to prove more than the evidence can bear. The careful claim is not that Canada is definitively a scarcity civilization. The careful claim is this:

The housing crisis can be interpreted as the clearest measurable expression of a broader shift from builder-oriented provision toward administratively mediated scarcity.

That sentence carries the ambition of the chapter without outrunning the proof.

The interpretation also helps explain why the effects of the housing system feel so broad. A society that can no longer reliably translate demand into housing often struggles in related domains as well: infrastructure delays, project overhang, procedural accumulation, and a widening gap between technical ability and institutional delivery. Housing does not prove all of that by itself. But because housing is ordinary and measurable, it makes the pattern hard to dismiss.

The interpretation limit matters here. This chapter does not claim that one housing argument exhausts the meaning of Canada, or that every failure of state capacity can be read directly out of housing alone. It claims something narrower: if one wants the clearest measurable domain in which to observe a shift away from provision and toward managed scarcity, housing is the strongest candidate assembled by this book.

This chapter is also falsifiable at the level appropriate to interpretation. If housing had remained broadly provision-oriented despite thicker administration, the broader reading would weaken. If the institutional thickening described earlier had not produced persistent economic consequences, the interpretive bridge would weaken. If ordinary housing delivery still functioned as a high-throughput system under pressure, this chapter’s larger inference would weaken. In that case, housing would look more like an isolated policy failure than a revealing surface of a broader turn. But the pattern assembled across the earlier chapters points in the other direction.

That is why the interpretive frame belongs here and not earlier. Only after the measurable chain has been built can the broader reading be offered responsibly. The empirical chapters showed the mechanism. This chapter asks what that mechanism may mean.

And once that interpretive frame becomes visible, the final question of the book changes. The issue is no longer merely diagnostic. It becomes political and institutional.

If housing is the clearest measurable surface of a broader shift toward managed scarcity, then the remaining question is whether that shift will continue to define the country — or whether the country will deliberately recover a builder logic.

That is the choice the final chapter takes up.

👉 “The Housing Scarcity Regime (P2)” https://skillsgaptrainer.com/the-housing-scarcity-regime-part-2/

That does not guarantee utopia. It does not erase trade-offs. It does not eliminate the complexity of modern urban life. But it would change the direction of the system. And direction is what matters most when a society has spent decades moving the wrong way.

This chapter is not the place for a new proof dump. The proof burden has already been carried by the earlier chapters. The final task here is narrower: to state the benchmark clearly enough that the reader can distinguish real reform from mere adaptation. If supply remains structurally blocked, if land remains politically throttled, if ownership remains the main gate to security, and if ordinary adult life remains dependent on entering scarce land early enough, then the regime has not truly changed.

So the final contrast is simple.

One path keeps the current regime in place: scarce land, defended values, deeper leverage, later adulthood, weaker family formation, and continued adaptation to exclusion.

The other path aims at renewal: more throughput, more housing, more normal price formation, more ordinary access to adult life, and a country that makes security less dependent on owning scarce land early enough.

That is the choice after managed scarcity.

And it is the choice this book has been trying to make visible from the beginning.